✂️ Time to buy more stocks? Lessons from past Fed cuts

📚 Interest rate theories

After a brief calm in the markets, last week came a burst of activity. Stock markets surged, with some breaking new records. Bitcoin rallied. US companies rushed to raise funds as bond yields fell.

All these happened after the US Federal Reserve cut interest rates. It’s a significant event – since 2020, America’s central bank has kept borrowing costs high to tame inflation.

Rate cuts mean loans become cheaper → companies and households become more willing to borrow to make big purchases → demand for goods and services go up → businesses make more money.

At the same time, lower interest rates also mean bond investors earn lower yields since they are the ones funding these loans. Bank savings account rates also fall, partly because banks will be earning less money from lending out the money you deposit.

For a more detailed explanation of why the Fed’s latest interest rate cut is significant, check out our 📱 Instagram post on this.

So how should we invest in the light of the Fed’s moves?

🔮What history says

The conventional wisdom is that stocks gain when interest rates are cut. That has so far played out.

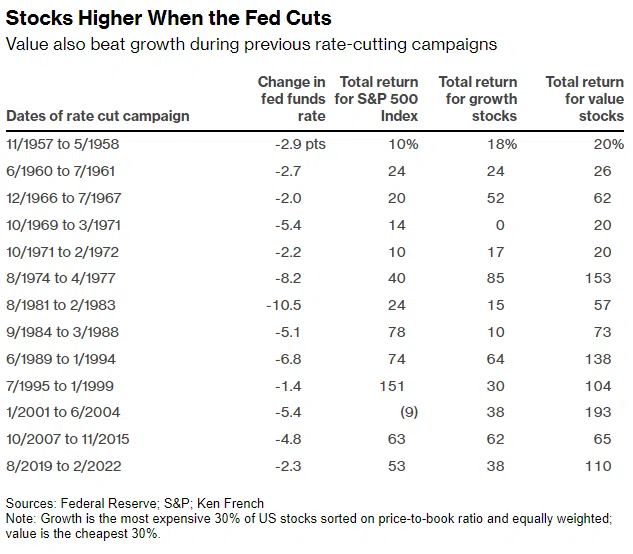

Since 1957, the S&P 500 index (a measure of the performance of the US’ largest companies) saw positive returns on 12 of 13 occasions that the Fed cut rates.

If stocks gain when interest rates are cut, it makes sense that the reverse would be true – that stocks fall when interest rates are hiked.

However, that didn’t happen. Instead of falling as expected, the S&P 500 also rose on 11 of the 13 occasions the Fed went on a rate-hike campaign since 1954.

That’s not the only confusing part. Conventional wisdom also suggests that growth stocks are more sensitive to rate changes. When interest rates are higher, it becomes more expensive for growing companies to borrow capital to fund their expansion. (There are other reasons, too, but those can get very technical.)

So when interest rates are hiked, buy value stocks; when they’re cut, buy growth stocks?

Again, the theory doesn’t quite pan out in reality. In recent rate-hiking campaigns since the 1990s, growth stocks beat value stocks three out of four times. And over the last 13 rate-cutting campaigns, value beat growth every time.

A crash course on value versus growth stocks:

Generally, there are two broad categories of stocks – value stocks and growth stocks.

The simplified explanation is that value stocks are ones that are priced below what they’re worth. You buy them cheap, then pray that prices go up before selling them and pocketing the difference. (We did an episode on this in our recent Investing with Choo 🌱.)

In contrast, growth stocks are expected to grow much faster than the market average. These tend to be technology companies where investors don’t mind paying high prices now because they may look cheap in hindsight. Think: Nvidia, Apple or Tesla.

✂️ What this means

The lesson here is that investing isn’t like physics 🔭. There are no strict laws that govern how markets are going to move. It is only in retrospect that people can say with certainty why markets moved the way they did.

Take for example this explanation from Bloomberg on why investors started moving money earlier in the month into value stocks, instead of growth, when they were expecting the Fed to cut rates:

“Wall Street traders are riding a rotation out of tech stocks that have contributed to most of this year’s bull run on expectations that the Fed lowering borrowing costs will juice economic growth, and create fresh winners like utilities and real estate.”

For investors thinking of chasing stocks now that the Fed has cut rates, here’s a (literal) word of advice from Nir Kaissar, founder of asset management firm Unison Advisors: Don’t 🙅.

In an opinion piece written for Bloomberg before the rate cuts, he gives his reasons.

“If stocks are paying any attention to short-term interest rates, there’s a good chance they have already digested most of the Fed’s expected policy easing.” In other words, you’re already late to the game.

Another reason not to go on a buying frenzy: If you want to increase your allocation to stocks, will you reduce your allocation when the Fed raises interest rates in the future?

If you do, you’d be giving up potential returns because recent history has shown that stocks climb whether the Fed raises or lowers interest rates. And if you don’t, then you’ll be maintaining a higher allocation of stocks, which means higher risk than you probably wanted.

The only alternative is timing the market just right – which Kaissar describes as “enticing, but a fantasy” 🧚.

One exception here is if you’ve been sitting on a pile of cash or Treasury bills and benefitted from high interest rates over the past years.

In that case, consider rebalancing your portfolio or make plans to optimise your yield, given that interest rates are expected to fall further. (Financial advisory firm MoneyOwl’s CEO makes a good case for not chasing yields in things you don’t understand.)

Otherwise, commit to your portfolio allocation – one that caters to your appetite for risk – and don’t let emotions or FOMO get in the way.

Kaissar writes: “As for the Fed, it’s probably best to ignore its interest rate moves when deciding how much to allocate to stocks.”

TL;DR

-

Conventional wisdom suggests that stocks, especially growth ones, do well when rates are cut

-

But reality has played out differently. In the past 13 rate hikes, stocks instead rose on 11 occasions

-

Value, rather than growth stocks, have performed better when rates are cuts

-

For most investors, it’s probably best to ignore interest rates when deciding how much to allocate to stocks