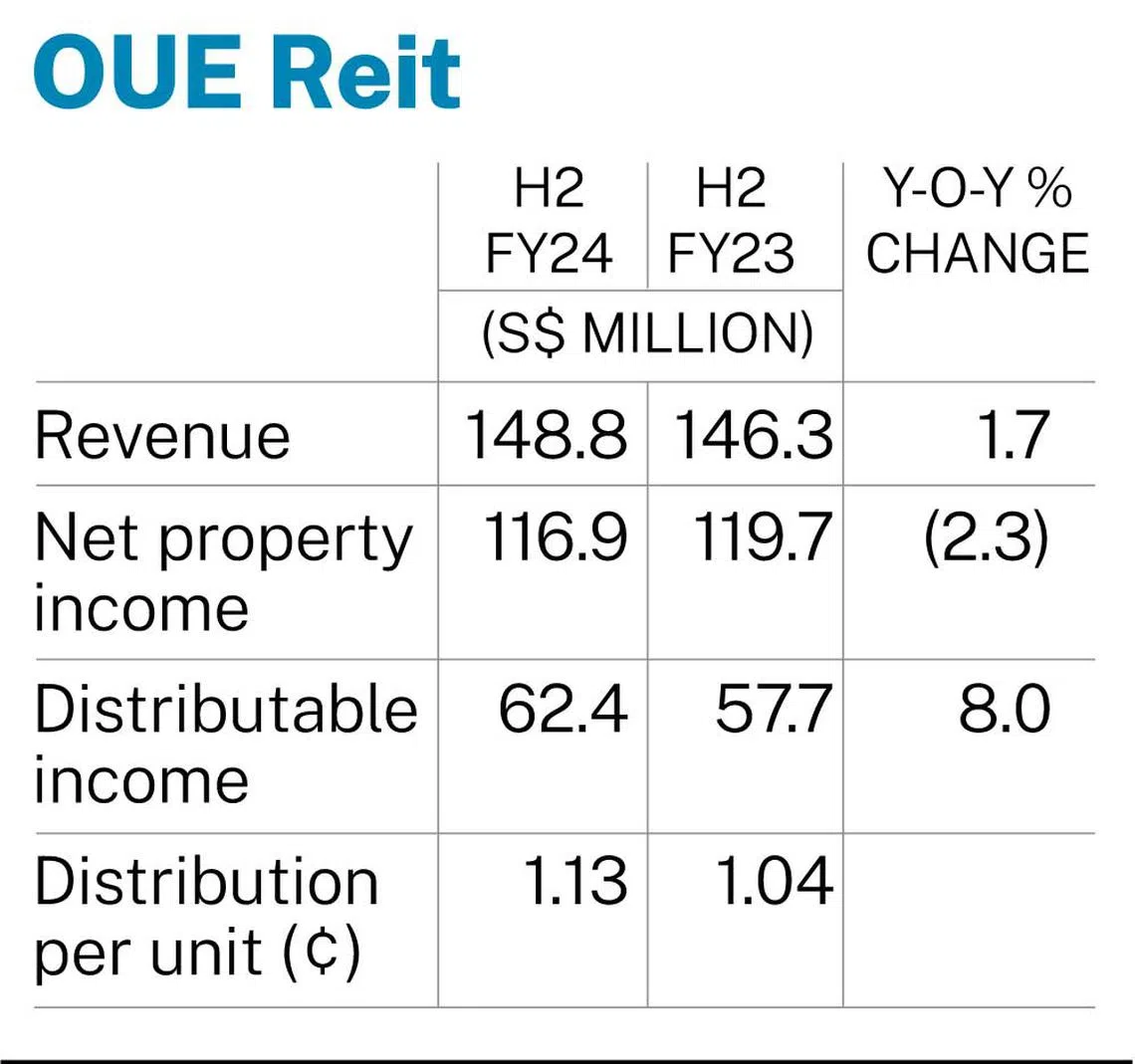

THE distribution per unit (DPU) for OUE Real Estate Investment Trust (Reit) rose 8.7 per cent to S$0.0113 for the second half of its financial year ended Dec 31, 2024, from S$0.0104 in the year-ago period, its manager said in a bourse filing on Thursday (Jan 23).

This came as revenue increased 1.7 per cent on the year to S$148.8 million, from S$146.3 million in the corresponding period in the prior year.

The growth was mainly due to the stable operational performance of the Reit’s Singapore office portfolio, as well as the successful asset enhancement of Crowne Plaza Changi Airport, which was completed in December 2023, its manager pointed out.

On the other hand, net property income (NPI) for the half year slipped 2.3 per cent to S$116.9 million, from S$119.7 million in H2 FY2023.

This was attributed to the upward revision of prior years’ property tax for Hilton Singapore Orchard and Crowne Plaza Changi Airport.

Adjusting for this revision, NPI would have recorded a year-on-year (yoy) increase of 0.3 per cent in H2 FY2024, it noted.

BT in your inbox

Start and end each day with the latest news stories and analyses delivered straight to your inbox.

The Reit manager added that the share of joint venture results from OUE Bayfront, which also contributes to NPI, doubled in the six-month period to S$26 million, mainly due to fair value gains.

The amount available for distribution for H2 2024 grew 3.7 per cent on the year to S$59.9 million. This was achieved despite its higher finance cost, which was offset by the payment of 50 per cent base management fee in units in Q4 FY2024 and the removal of working capital retention, the manager noted.

Including the release of the remaining S$2.5 million capital distribution from the 50 per cent divestment of OUE Bayfront, the amount to be distributed to unitholders was S$62.4 million, marking an 8 per cent yoy increase from S$57.7 million.

The distribution for the period, comprising taxable income distribution, tax-exempt income distribution and capital distribution, will be paid on Mar 5, 2025, after books closure on Feb 4.

For the full year, the manager of the trust announced a DPU of S$0.0206, down 1.4 per cent from S$0.0209 in the year-ago period.

The amount to be distributed was S$113.7 million, a decrease of 1.4 per cent from S$115.3 million in FY2023.

Revenue expanded 3.7 per cent to S$295.5 million, from S$285.1 million a year ago, while NPI slipped a marginal 0.4 per cent to S$234 million, from S$235 million.

Its net asset value per unit stood at S$0.58 as at Dec 31, 2024.

OUE Reit comprises a commercial segment as well as a hospitality segment.

Committed occupancy of the Reit’s Singapore office properties remained healthy at 94.6 per cent as at end-December 2024, with full-year positive rent reversion of 10.7 per cent.

Said the manager: “Occupier sentiment is expected to remain weak due to global economic uncertainties, high fit-out costs and elevated interest rates.”

It added: “However, below-historical-average office supply in the Core Central Business District (Grade A) over the next four years, combined with anticipated interest rate cuts, is likely to bolster corporate confidence in expansion in 2025.”

Citing CBRE forecasts, it noted that rents in the area will grow by 2 per cent for the full year in 2025, against 2024’s modest 0.4 per cent growth, “supported by the ongoing flight-to-quality trend”.

As for its hospitality segment, the manager highlighted that tourism recovery is expected to continue, though the outlook for FY2025 remains cautious amid more affordable regional competitors, and the absence of high-profile concerts and meetings, incentives, conferences and exhibitions events.

Units of OUE Reit closed flat at S$0.30 on Thursday, before the announcement.