“BUY now, pay later” (BNPL) will remain as one of the payment methods in Singapore, together with digital wallets and credit and debit cards, according to Worldpay’s 2024 Global Payments Report.

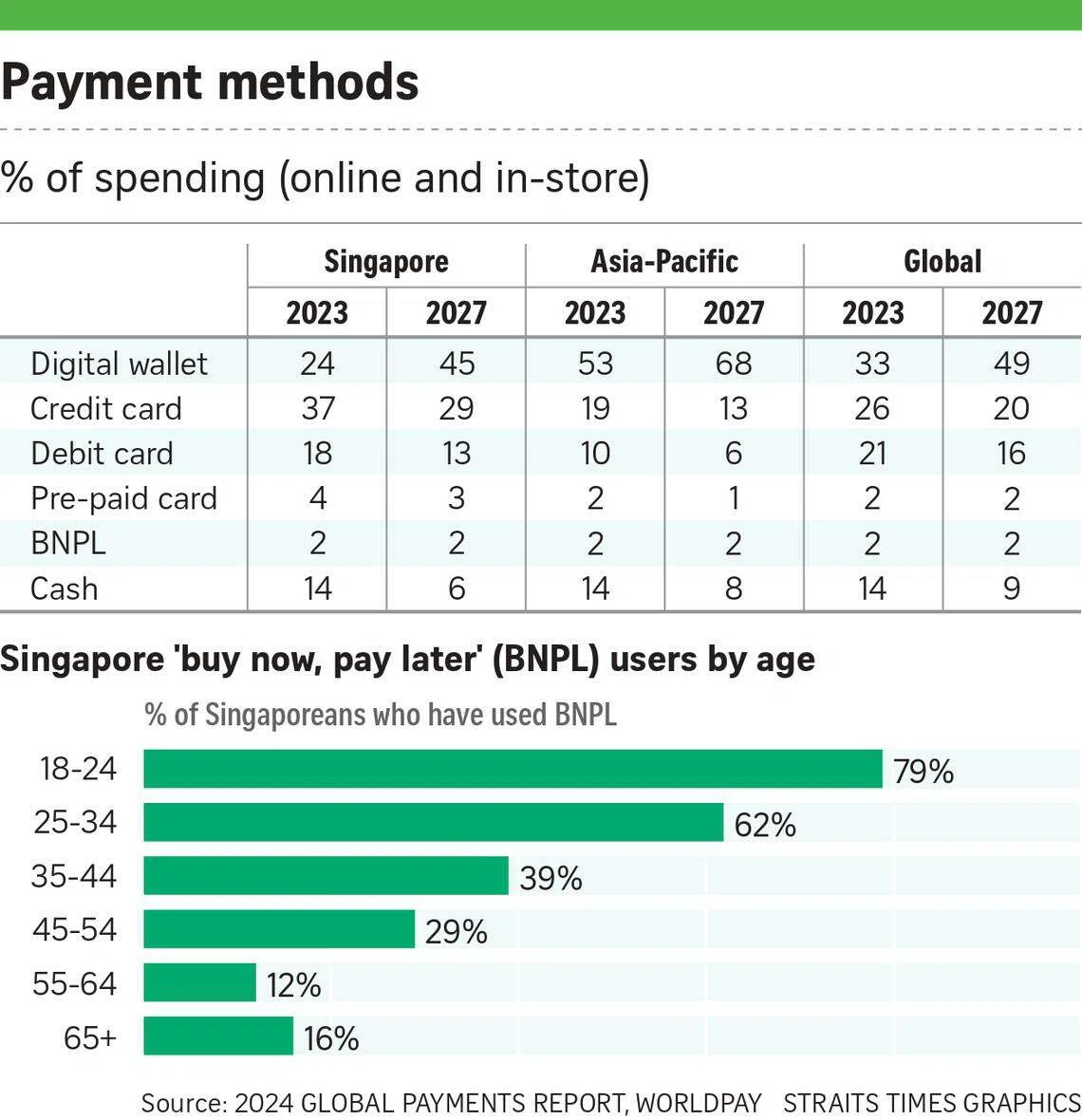

The payments technology and solutions company said that by 2027, BNPL will account for 2 per cent of total spending – e-commerce and point of sale transactions – unchanged from 2023.

In comparison, the use of digital wallets, such as Apple Pay, Google Wallet, GrabPay and ShopeePay, is expected to increase year over year. By 2027, digital wallets will account for 45 per cent of total spending – e-commerce and point of sale transactions – from 24 per cent in 2023.

The total spending via digital wallets will grow from S$41 billion in 2023 to S$89 billion in 2027, Worldpay said.

The firm said that by 2027, credit card usage will drop to 29 per cent of total spending (from 37 per cent in 2023) while debit cards will account for 13 per cent of all spending (from 18 per cent in 2023).

In 2023, Singapore consumers spent S$3.4 billion online and in-store using BNPL services from third-party providers like Atome and Grab PayLater, banks and retailers.

A NEWSLETTER FOR YOU

Thrive

Money, career and life hacks to help young adults stay ahead of the curve.

The Worldpay survey found that Gen Z, those between 18 and 24 years old, and young millennials between 25 and 34 years old, were among the bigger users of this method.

Seventy-nine per cent of Gen Zers and 62 per cent of young millennials in Singapore have used BNPL.

The percentage drops progressively across the older age cohorts, with 39 per cent of older millennials between 35 and 44 years old; 29 per cent of Gen Xers aged 45 to 54; and 12 per cent of those aged 55 to 64, having tried out BNPL here.

Phil Pomford, general manager for Worldpay’s global enterprise e-commerce team in the Asia-Pacific region, said Gen Zers and millennials are attracted to the ease and convenience that BNPL platforms offer.

He said they like the option of spreading their payments over a few months and not having to pay interest for doing so.

Zennon Kapron, director of Singapore-based fintech research and consulting firm Kapronasia, said Gen Zers and millennials are more open to alternative financing options and often look for manageable ways to budget for bigger purchases.

They tend to use BNPL to pay for electronics and high-value gadgets because these products are more expensive, and fashion and beauty products because people buy and change them more frequently, he said.

Increasingly, Kapron said BNPL is also being used to fund educational expenses, such as online courses.

But 2023 has been challenging for BNPL players as they faced headwinds, including rising interest rates and impending tighter regulation for the sector, said Pomford.

Countries, most recently Australia, want to regulate this space to protect consumers from falling too deeply into debt.

Competition is also heating up as other players, such as the banks, look to capture some of the BNPL market, he added.

In Singapore, OCBC was the first to introduce a card with BNPL-like features, the NXT credit card.

UOB followed with SmartPay, Standard Chartered Bank with EasyPay, Maybank with FlexiPay, DBS with My Preferred Payment Plan and HSBC with its Pay in Instalments Payment Plan.

Kapron said the banks have an edge over third-party BNPL firms because they can leverage their lending experience and customer and deposit base. He added that other large traditional players like Singtel have come in with their own BNPL services.

The telco’s BNPL scheme, Singtel PayLater, allows consumers to pay for mobile phones, home appliances and personal electronics in interest-free instalments.

Even as more players join the market, at least a dozen third-party BNPL firms have ceased operations in 2023.

Worldpay said they included Zest in India, Laterpay in Germany, myIOU in Malaysia, Openpay and LatitudePay in Australia, and Pace in Singapore.

LatitudePay was one of the BNPL providers that were expected to get BNPL accreditation in Singapore, but it shut its operations here and in Malaysia in April.

It stopped accepting new customers from Apr 4 and halted purchases on its platform after Apr 19.

ShopBack also discontinued its BNPL service, PayLater, in Singapore on Mar 22.

There are currently four third-party BNPL providers here – Atome, Grab, SeaMoney and Abnk – operating with the accredited Trustmark since May 1. THE STRAITS TIMES