Marco Polo Marine CEO increases stake; ESR Reit buys back 5 million units

OVER the five trading sessions from Feb 7 to 13, institutions were net buyers of Singapore stocks, leading to a net institutional inflow of S$63 million, partially reversing the net outflow of S$169 million in the preceding five sessions.

This brings the net institutional outflow for the year to Feb 13 to S$633 million.

Institutional flows

The stocks that led the net institutional inflow over the five sessions included Singtel, Seatrium, Singapore Exchange (SGX), CapitaLand Integrated Commercial Trust, CapitaLand Ascendas Real Estate Investment Trust (Reit), Yangzijiang Shipbuilding, CapitaLand Investment, Yangzijiang Financial, Rex International and Suntec Reit.

Meanwhile, the counters that led the net institutional outflow included OCBC, DBS, Keppel, Sembcorp Industries, Mapletree Industrial Trust, UOB, Frasers Centrepoint Trust, Sats, ComfortDelGro and Hongkong Land.

Consequently, over the five sessions, telecommunications and industrials recorded the highest net institutional inflow, while financial services and utilities posted the most net institutional outflow.

Singtel booked S$112 million of net institutional inflow over the five sessions, bringing its net institutional inflow for the year to Feb 13 to S$235 million.

BT in your inbox

Start and end each day with the latest news stories and analyses delivered straight to your inbox.

On Feb 7, the telco announced that its regional data centre arm, Nxera DCT, secured a S$643 million five-year green loan to develop a 58-megawatt data centre in Singapore.

The loan will fund the development and capital expenditure of DC Tuas, which is intended to be the “most hyper-connected green data centre” and have the highest power density in the country.

The data centre was awarded the Green Mark Platinum certification, reinforcing the group’s commitment to sustainable design and operations.

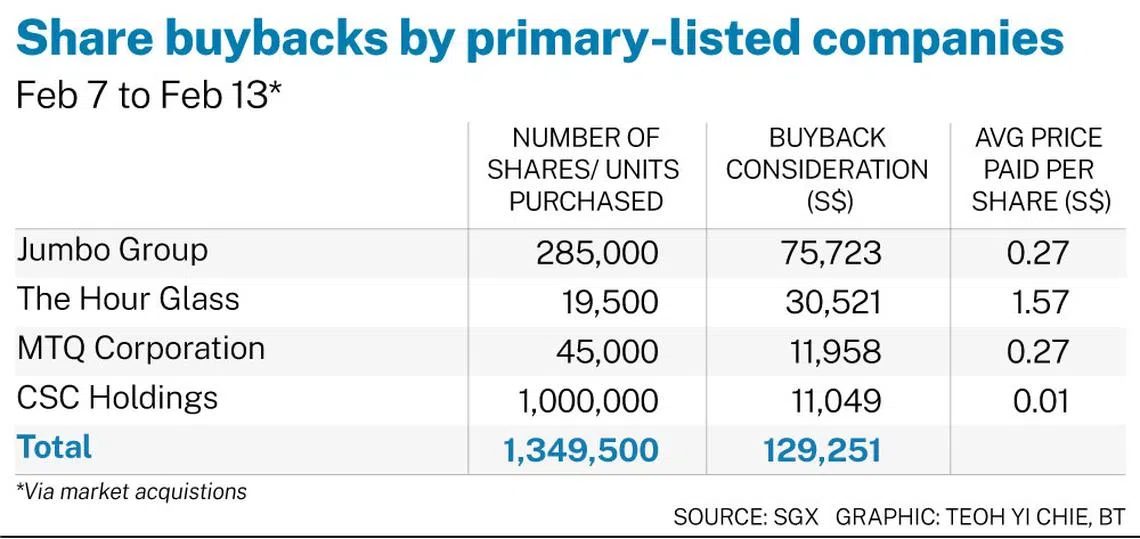

Share buybacks

Over the five sessions, four primary-listed companies conducted buybacks, with a total consideration of S$129,251, similar to the S$130,882 filed during the preceding five ones.

The decline in buyback filings is seasonal, attributable to the busy schedule for releasing full-year financial statements in February. As a best practice, companies should avoid buying back their shares in the month immediately preceding the release of their full-year financial statements.

ESR Reit

ESR Reit’s management bought back five million units of the investment trust on Feb 11 at an average price of S$0.248 per unit.

This took the number of units acquired on the current buyback mandate to 24 million, or 0.31 per cent of the outstanding issued units. The trust reported its FY2024 results on Jan 24.

As at Dec 31, 2024, ESR Reit held interests in a diversified portfolio of business parks, as well as properties across the general industrial, high-specifications industrial and logistics sectors.

The trust’s total assets stood at about S$6 billion, comprising 72 properties across Singapore, Australia and Japan, as well as investments in three Australia property funds.

On Jan 27, ESR Reit’s manager announced that it entered a contract to divest properties at 1 Third Lok Yang Road and 4 Fourth Lok Yang Road for around S$6.8 million, representing a 3.5 per cent premium above their valuation.

Following the divestment, the trust’s portfolio will comprise 70 properties at the end of Q1 2025.

Net proceeds from the sale will be used to repay borrowings and finance acquisitions, asset enhancements and redevelopments, as well as for general working capital.

Since 2022, ESR Reit’s management has pursued a “4R strategy”. It has been focused on recapitalising the balance sheet, rejuvenating the asset portfolio, recycling capital and reinforcing the sponsor’s support.

Adrian Chui, the chief executive officer of the manager, said this strategy has led to income growth for the investment trust. It is expected to translate into higher net property income and distribution per unit, as well as improved asset and earnings quality.

Director transactions

The five trading sessions saw less than 40 director interests and substantial shareholdings filed for more than 20 primary-listed stocks. Directors or CEOs filed 12 acquisitions and one disposal, while substantial shareholders filed eight acquisitions and two disposals.

Marco Polo Marine

On Feb 11, Marco Polo Marine executive director and CEO Sean Lee acquired one million shares at an average price of S$0.054 per share.

This took his total interest in the regional integrated marine logistics company to 4.8 per cent, from 4.78 per cent. His preceding acquisition was on Dec 4, with two million shares acquired at S$0.053 apiece.

Lee has been the company’s chief executive since September 2007. He is responsible for setting the business strategies and directions for the group, and managing its business operations. He has gradually increased his total interest in the company from 0.23 per cent as at end-2017.

Marco Polo Marine reported revenue of S$123.5 million for FY2024 (ended Sep 30), down from S$127.1 million in FY2023. Its ship chartering segment continued to drive growth, benefiting from higher charter rates and robust demand from the offshore oil-and-gas and renewable energy sectors.

Conversely, its shipyard segment’s revenue was affected by the construction of a new commissioning service operation vessel (CSOV), which led to lower ship repair volumes and reduced third-party shipbuilding activities.

Last week, the management of Marco Polo Marine hosted a broad mix of market participants on Wind Archer, the new CSOV, which is designed to meet Asia’s growing demand for support vessels in the offshore wind farm industry.

The S$60 million vessel is equipped with the latest walk-to-work motion-compensated gangway for safe personnel transfer, and a 3D motion-compensated crane for cargo transfer.

It features state-of-the-art green technology, including a hybrid battery-based energy storage system that reduces carbon emissions by 15 to 20 per cent, and is designed to be future-ready for methanol fuel use.

The vessel can accommodate up to 110 people. Its amenities include a gym with windows, a cinema room, spacious kitchen facilities and multiple gathering rooms.

Wind Archer will soon set sail to be deployed across various offshore wind farm projects in Taiwan. The charter rates are kept confidential due to the competitive nature of the growing offshore wind sector.

Marco Polo Marine’s strategic pivot towards the renewable energy sector has helped to diversify its customer base, in addition to increasing its asset utilisation. Its net asset value stood at S$201.1 million as at FY2024, up from S$183.9 million in FY2023.

The company has a cash position of S$68.8 million, with net cash amounting to S$35.8 million after accounting for borrowings.

Marco Polo Marine is headquartered in Singapore. Meanwhile, its shipyard is in Batam and occupies more than 34 hectares of land. In FY2024, the shipyard operated at an average utilisation rate of 91 per cent, compared with 84 per cent in FY2023.

The company’s fourth dry dock commenced construction in May 2024, and is expected to be completed in the first half of this year. The new dry dock will be used for building, maintaining and repairing ships, which will further strengthen Marco Polo Marine’s capabilities. Revenue recognition from the dry dock is expected to start in H2 2025.

The remainder of Marco Polo Marine’s fleet – which includes vessels such as offshore support vessels, maintenance work vessels, tugboats and barges – supports its operations in the offshore market.

Travelite

On Feb 5, Travelite executive chairman Thang Teck Jong acquired 1,024,200 shares at an average price of S$0.174 per share. This increased his total interest in the brand management company to 65.71 per cent, from 64.63 per cent.

He has been growing his total interest since November, when it was at 61.68 per cent.

Thang formulates the group’s strategic directions and expansion plans. He founded the group in 1986, and has been instrumental in its growth and development.

Casa

Casa’s independent non-executive director Wee Chow Hou has been building a direct interest in the investment holding company recently.

The company is a leading distributor of home appliances in Singapore, with an extensive distribution network consisting of more than 300 established retailers islandwide.

For FY2024 (ended Sep 30), the company’s revenue fell 11.7 per cent to S$20.7 million, primarily due to a market slowdown and normalisation of sales volumes. Despite this, its gross margin improved to 44.4 per cent, from 43.8 per cent in FY2023, on the back of cost management and product mix.

Dr Wee’s first acquisition was on Feb 3, when he bought 70,000 shares at S$0.109 per share. This was followed by a purchase of 129,000 shares at S$0.106 apiece on Feb 4, and 95,200 shares at S$0.106 per share on Feb 6.

These acquisitions took his direct interest in the company to 0.17 per cent.

Dr Wee was appointed to Casa’s board in March 2022. He is an emeritus professor at Nanyang Technological University (NTU) and an honorary fellow of the Singapore University of Social Sciences.

He has held various senior positions at both NTU and the National University of Singapore, and consulted for more than 350 major organisations globally. He has also served as an independent director for several listed companies in Singapore.

The writer is the market strategist at SGX. To read SGX’s market research reports, visit sgx.com/research.